EPS

- Organic EPS CAGR target: +10-12%

- Accelerate EPS compounding through aggressive M&A activities

Our basic Management Policy, Management Strategy, Medium-Term Management Plan, and competitive strengths

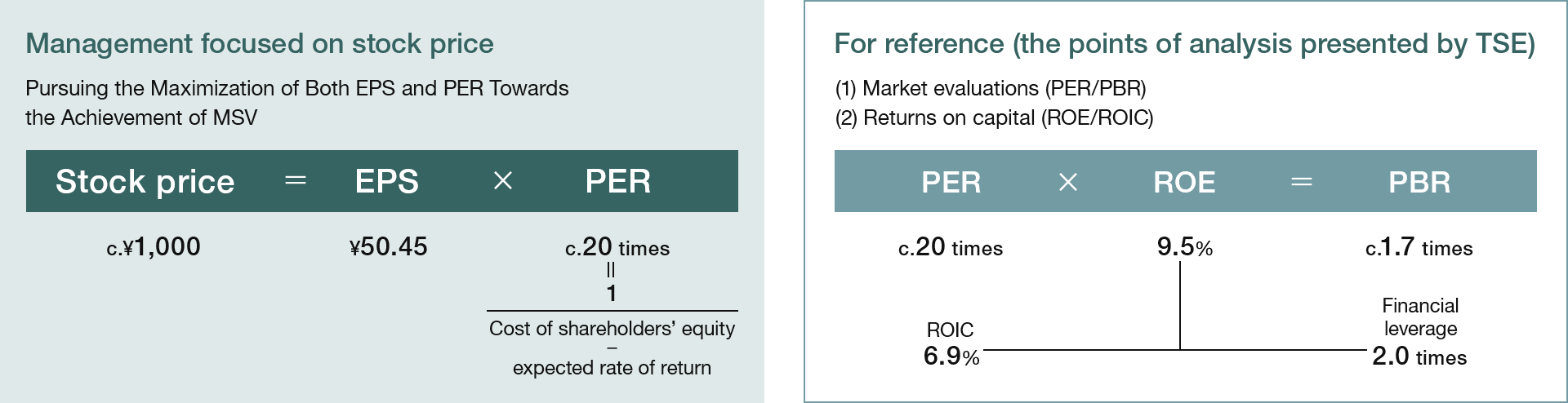

We are pursuing our sole mission of MSV through the maximization of EPS and PER. We practice management with a focus on our stock price, which is the outcome of the pursuit of MSV.

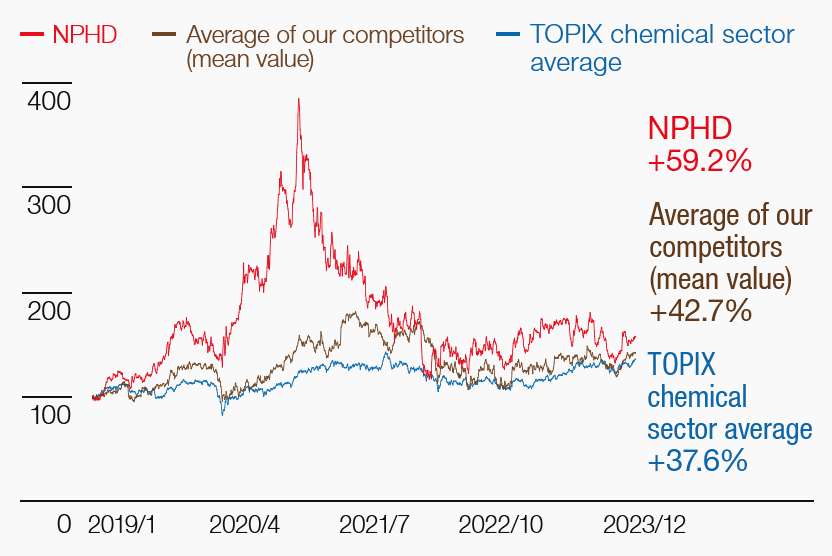

Over the past five years, our stock price has outperformed the TOPIX chemical sector average and the average of our competitors, bolstered by robust EPS growth. However, our stock price declined despite the growth in EPS, prompting us to carry out an analysis that takes into account macroeconomic factors, sector trends, and our own analysis of stock price trends.

Moving forward, we aim to achieve MSV by focusing on sustainable EPS compounding and elevating capital markets’ expectations.

*1 Source: FactSet, Bloomberg

*2 The stock prices were indexed with the closing price on January 1, 2019 as 100

*3 The average of competitors is the average of indexed stock prices of SherwinWilliams, BASF, Asian Paints, PPG, AkzoNobel, Berger Paints, Axalta Coating Systems, SKSHU Paint, Kansai Paint, TOA Paint, and Asia Cuanon Technology

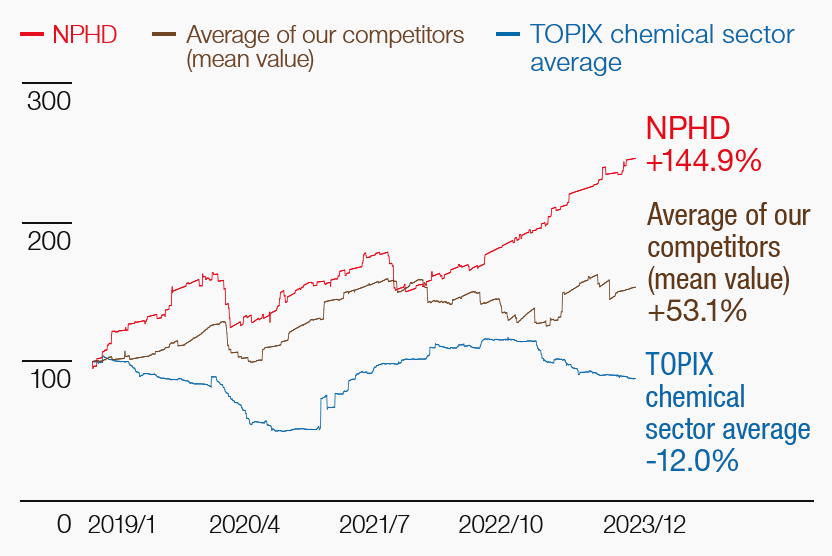

*1 Source: FactSet, Bloomberg

*2 The stock prices were indexed with the closing price on January 1, 2019 as 100

*3 Average of our competitors is the average of indexed stock prices of SherwinWilliams, BASF, Asian Paints, PPG, AkzoNobel, Berger Paints, Axalta Coating Systems, SKSHU Paint, Kansai Paint, TOA Paint, and Asia Cuanon Technology

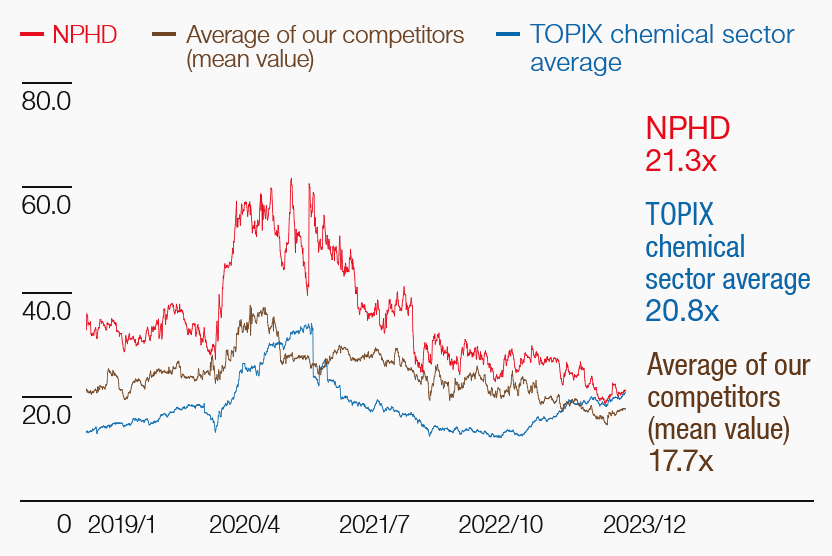

*1 Source: FactSet, Bloomberg

*2 Average of our competitors is the average stock price of Sherwin-Williams, BASF, Asian Paints, PPG, AkzoNobel, Berger Paints, Axalta Coating Systems, SKSHU Paint, Kansai Paint, TOA Paint, and Asia Cuanon Technology

| Five-year trend (2019-2023) | Three-year trend (2021-2023) | One-year trend (2023) | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Stock price | EPS | PER | Stock price | EPS | PER | Stock price | EPS | PER | |

| NPHD | +59.2% | +144.9% | -11.3x | -62.1% | +56.6% | -25.6x | +8.6% | +27.5% | -3.7x |

| Average of our competitors | +42.7% | +53.1% | -3.5x | -17.0% | +21.8% | -9.6x | +13.5% | +11.0% | -4.6x |

| TOPIX chemical sector average | +37.6% | -12.0% | +7.5x | +9.1% | +70.3% | -11.6x | +25.4% | +63.6% | +8.1x |

As analyzed below, while our EPS has significantly increased over the past five years, the rate of change in our PER has been trending downward compared to the TOPIX chemical sector average and the average of competitors, even though the absolute level of PER is not low.

We believe that the main factors contributing to this decline in PER are: (1) market anxieties over China-related risks; (2) an underestimation of our growth potential; and (3) our aggressive M&A strategy being evaluated as high risk. We are working to alleviate these concerns and evaluations. Furthermore, we are committed to accelerating the sustainable EPS compounding through both organic and inorganic growth towards achieving MSV.

* The stock price is as of June 30, 2024; the EPS, ROE, ROIC, and financial leverage are based on the 2023 results; and the PER and PBR are as of June 30, 2024.