Font Size

1. Front Cover

Good afternoon, everyone. I’m Yuichiro Wakatsuki, Co-President of Nippon Paint Holdings.

Thank you for joining us today as we discuss our fourth-quarter and full-year FY2024 financial results, along with our financial outlook for FY2025.

As is customary for our earnings calls in the second and fourth quarters, members of the press are also in attendance today.

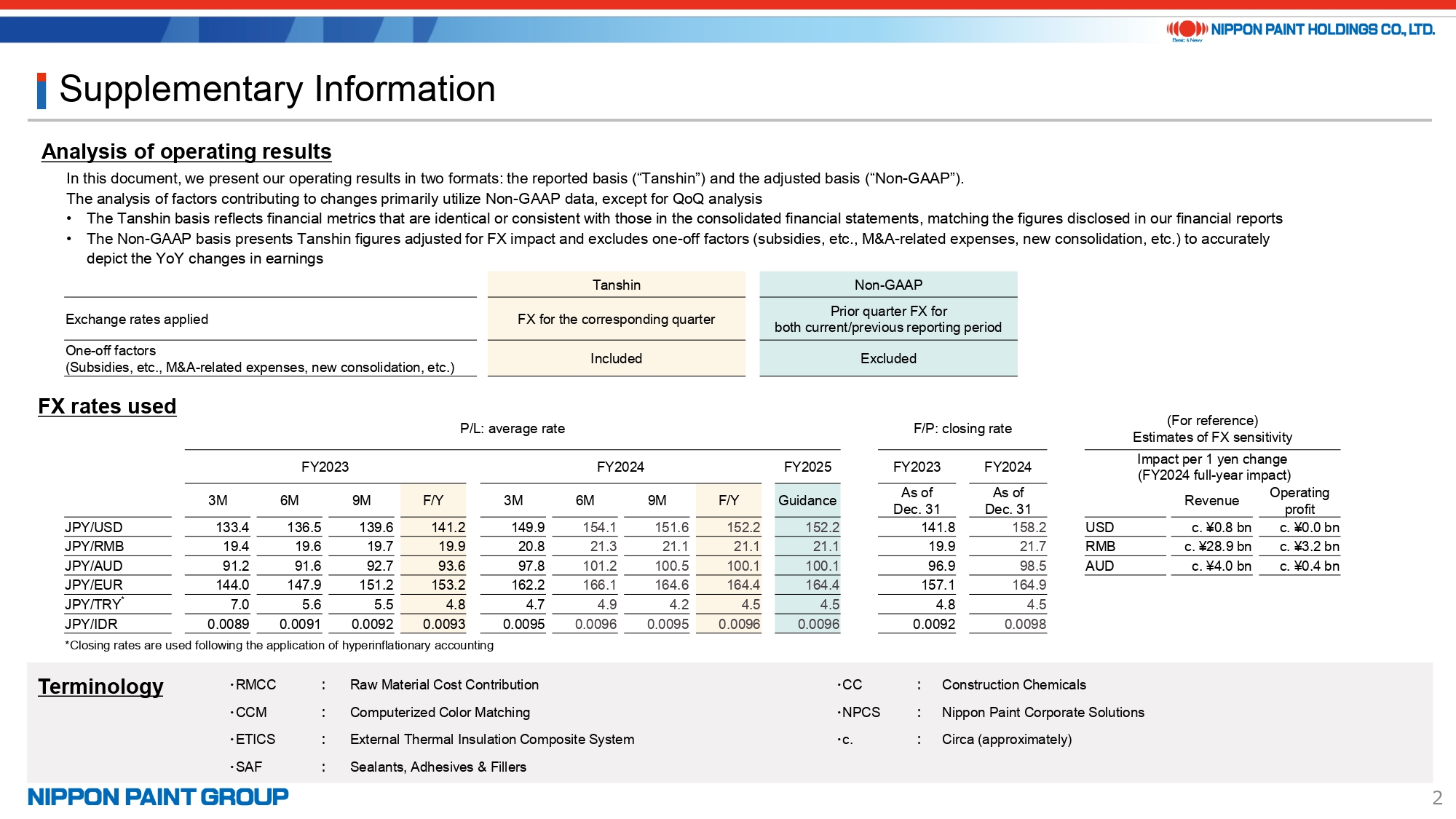

2. Supplementary Information

Before reviewing our financial performance, I’d like to highlight that our FY2025 guidance is based on the same exchange rates used for our FY2024 results.

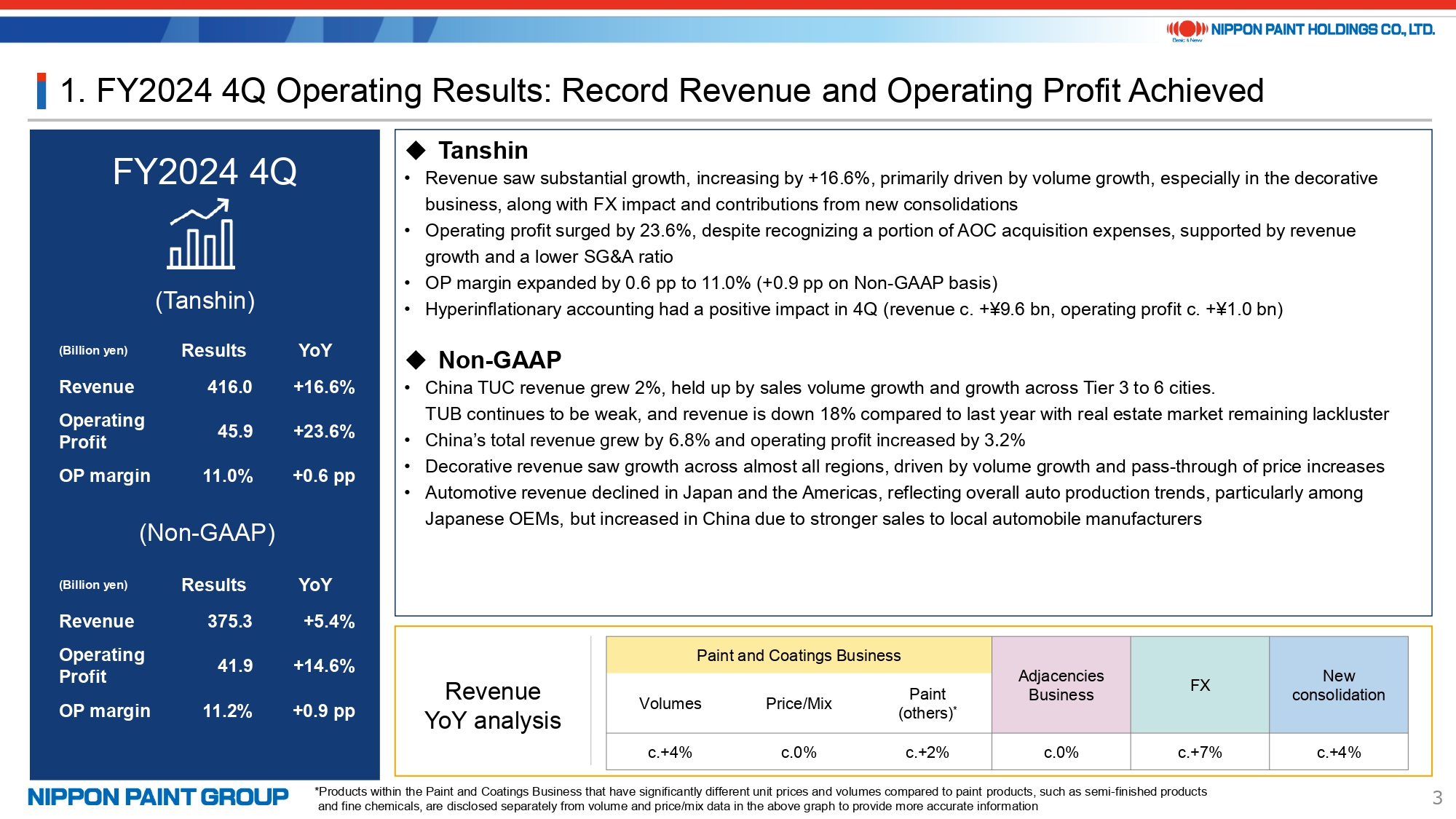

3. FY2024 4Q Operating Results: Record Revenue and Operating Profit Achieved

Now, let me begin by summarizing the key highlights of the fourth quarter of FY2024.

On a Tanshin basis, revenue increased by 16.6% year-on-year to 416.0 billion yen, while operating profit rose by 23.6% to 45.9 billion yen, setting new record highs for both revenue and operating profit in the fourth quarter. This strong performance was driven by the outstanding efforts of our teams across all regions in navigating the seasonally subdued demand typically seen toward the year-end. As shown in the lower section of the presentation, key factors contributing to revenue growth included higher paint sales volumes, contributions from our other paint business, favorable foreign exchange impacts, and new consolidations. Meanwhile, price and mix impacts remained flat overall compared to the same period last year.

On a Non-GAAP basis, which excludes FX impact, new consolidations, and other one-off factors, revenue grew by 5.4%, while operating profit increased by 14.6%. In NIPSEA China’s decorative paints business, TUC revenue rose by 2%, whereas TUB revenue declined by 18%. However, overall operating profit for NIPSEA China increased, driven by revenue growth and improvements in the SG&A expense ratio.

In the automotive segment, revenue declined in Japan and the Americas due to reduced automobile production by Japanese OEMs. In contrast, automotive revenue in China increased, supported by stronger sales to local automobile manufacturers.

Additionally, the operating profit margin improved year-on-year, increasing by 0.6 percentage points on a Tanshin basis and 0.9 percentage points on a Non-GAAP basis.

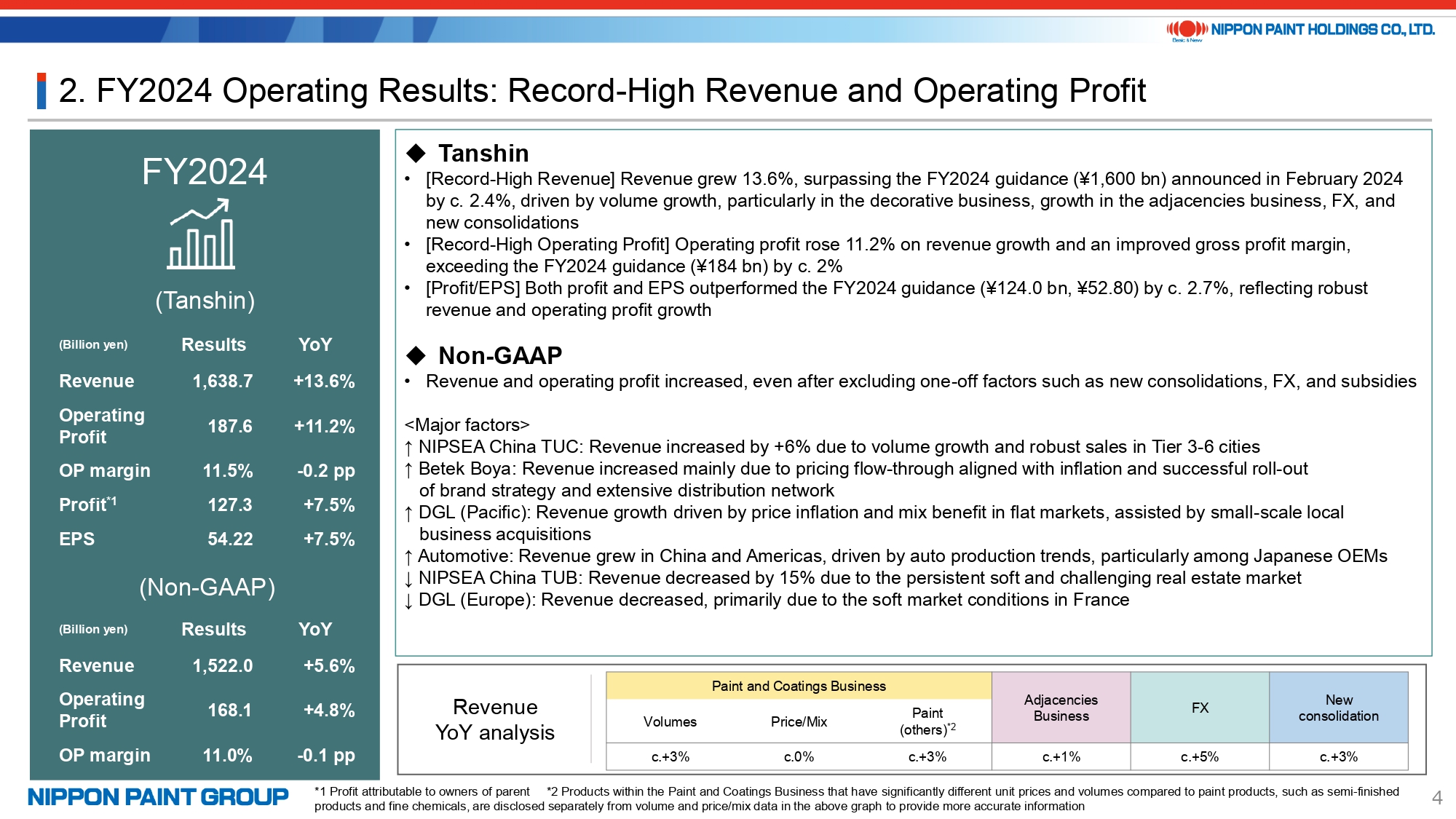

4. FY2024 Operating Results: Record-High Revenue and Operating Profit

Turning to our full-year 2024 performance, both revenue and operating profit reached new record highs. These results not only exceeded the FY2024 guidance announced last February but also surpassed the projections we shared during our earnings call last November.

On a Tanshin basis, revenue grew by 13.6%, while operating profit increased by 11.2%. On a Non-GAAP basis, which excludes FX impact, new consolidations, and other one-off factors, revenue rose by 5.6%, and operating profit grew by 4.8%. These strong results were achieved thanks to the outstanding efforts of our teams across all regions, despite operating in a highly challenging environment.

Our consolidated operating profit, both on a Tanshin and Non-GAAP basis, continued to be affected by hyperinflationary accounting in Türkiye. This adjustment reduced our FY2024 operating profit by approximately 3.2 billion yen. Despite this impact, we successfully maintained a double-digit operating profit margin even after accounting for hyperinflationary adjustments.

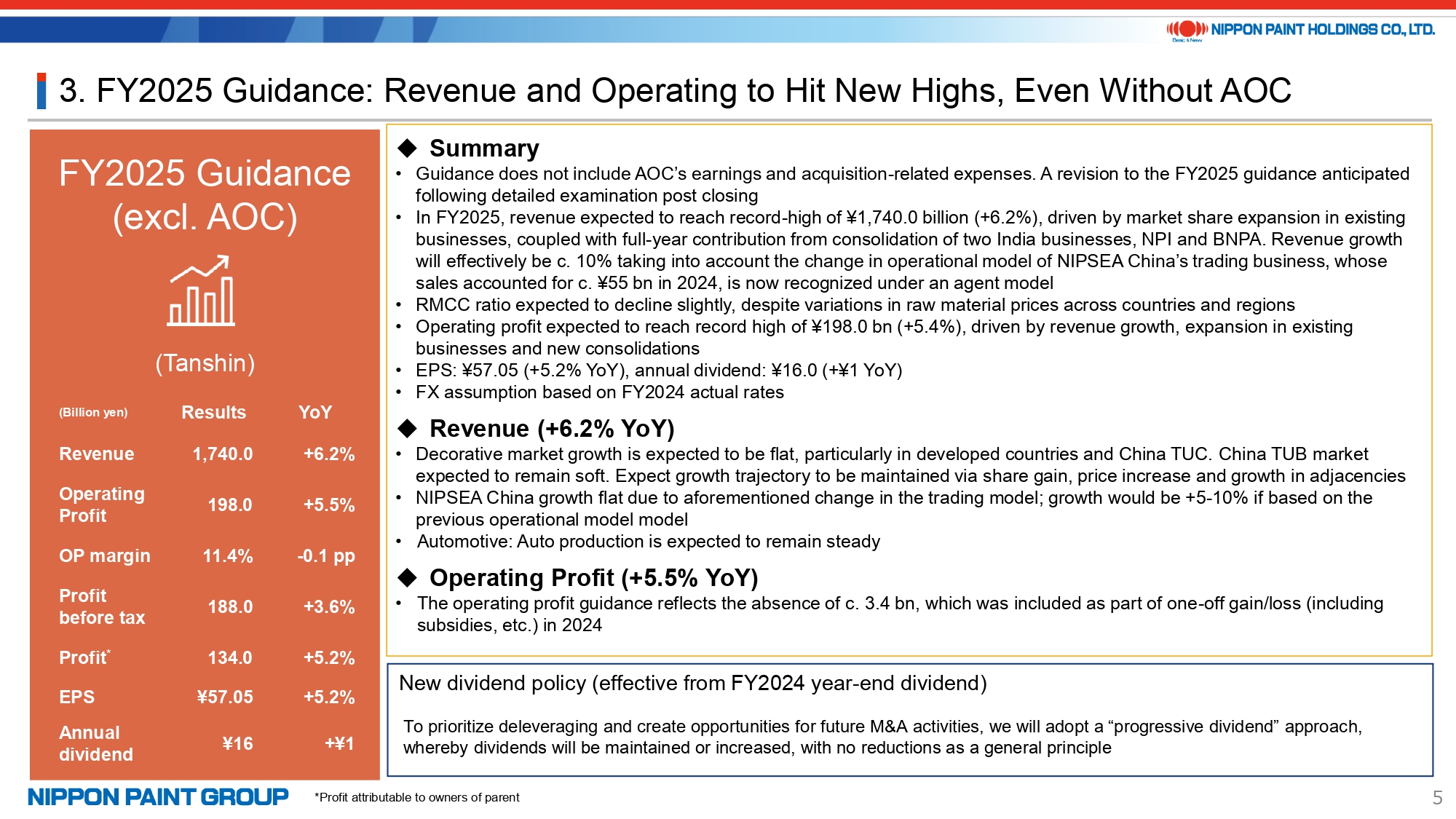

5. FY2025 Guidance: Revenue and Operating to Hit New Highs, Even Without AOC

Now, let’s turn to our FY2025 guidance.

First, I’d like to provide an update on the acquisition of AOC, which was announced last October. As noted on page 11 of the presentation, the fulfillment of closing conditions is progressing smoothly and could be completed as early as the end of February. However, due to the uncertainty surrounding the timing of regulatory approvals, our current guidance does not include AOC’s earnings or acquisition-related expenses.

Once the acquisition is finalized, we will make an official announcement and update our FY2025 guidance following a detailed post-closing review.

Regarding revenue, assuming exchange rates remain at FY2024 levels, we project consolidated revenue to grow by approximately 6% to a record high of 1,740 billion yen. This growth will be driven by expansion in our existing businesses through proactive market share initiatives, the strengthening of our adjacencies business, and the full-year contribution from our two newly consolidated India businesses, which were added in FY2024 but contributed only two months of earnings during the fiscal year.

NIPSEA China’s decorative business also includes a trading segment outside of the TUC and TUB categories. Previously, both purchase and sales amounts were recorded for this segment. However, starting this year, due to a change in the trading business’s operational model, we will only recognize the net amount. Considering the approximately 55.0 billion yen reported from this segment in FY2024, our effective consolidated revenue growth will be closer to 10%. On page 6 of the presentation, we have indicated that total revenue for NIPSEA China in FY2025 is expected to remain flat. However, on a like-for-like (Apple-to-Apple) basis, we anticipate 5–10% revenue growth for NIPSEA China in FY2025.

Operating profit is expected to increase by 5.5% to 198.0 billion yen. The FY2024 operating profit included approximately 4.1 billion yen in net one-off gains, comprising subsidies, AOC acquisition-related expenses, and other non-recurring items. The FY2025 guidance accounts for the absence of around 3.4 billion yen from these one-off gains/losses in FY2024. Adjusting for this, the underlying operating profit growth for FY2025 would effectively be 7.5%. The operating profit margin is projected to remain largely stable year-on-year, and EPS is forecasted at 57.05 yen.

When we announced the acquisition of AOC last October, we briefly mentioned our approach to dividends. The Board of Directors has now officially decided to adopt a progressive dividend policy as our fundamental approach. Given the expected significant increase in EPS following the AOC acquisition, our priority will be deleveraging and preparing for future M&A opportunities that can further enhance EPS, rather than strictly adhering to the conventional 30% dividend payout ratio.

For FY2025, we are forecasting an annual dividend of 16 yen, an increase of 1 yen from the previous year. As a general principle, this dividend forecast will remain unchanged even if we revise our FY2025 guidance after completing the AOC acquisition.

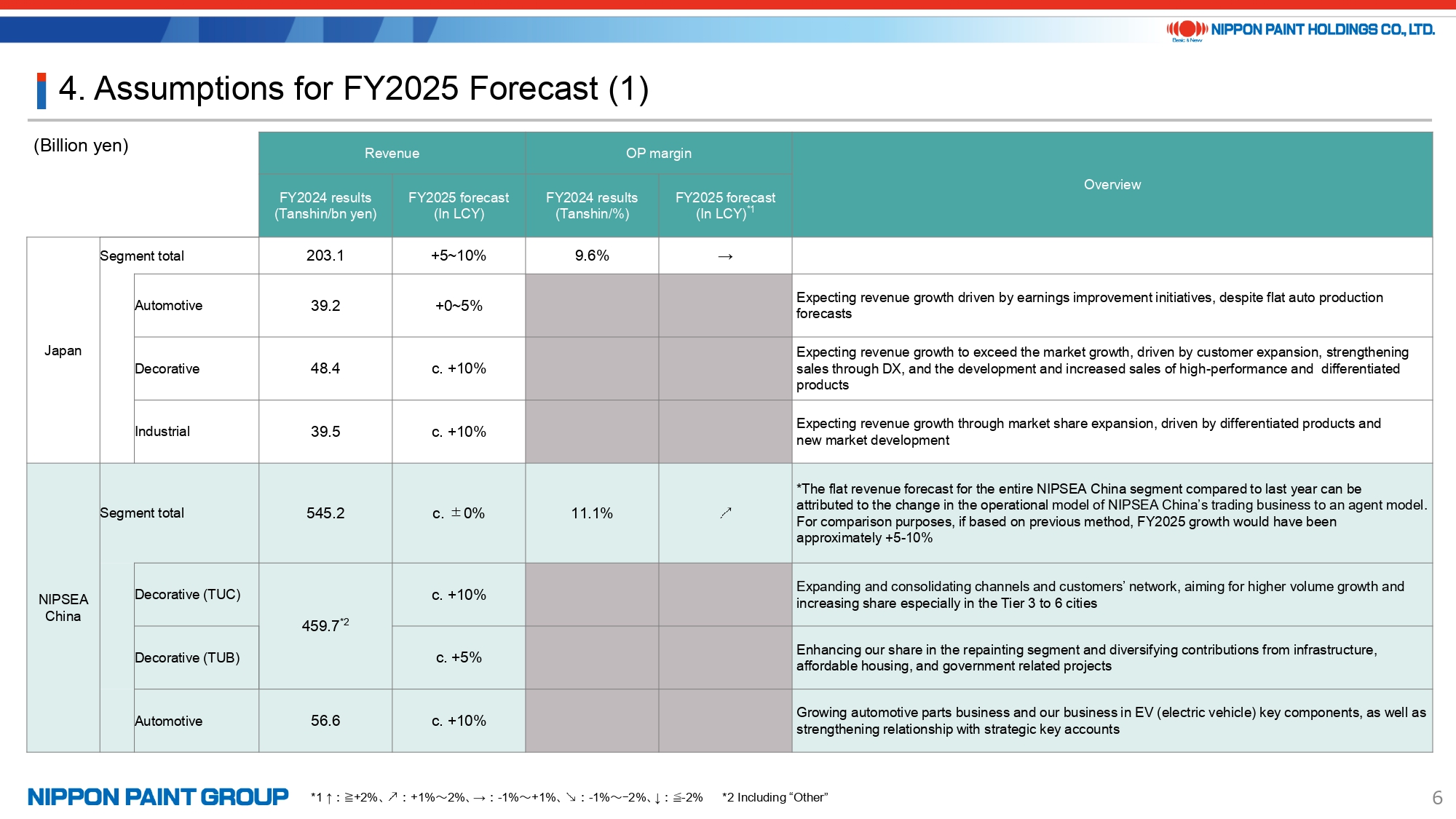

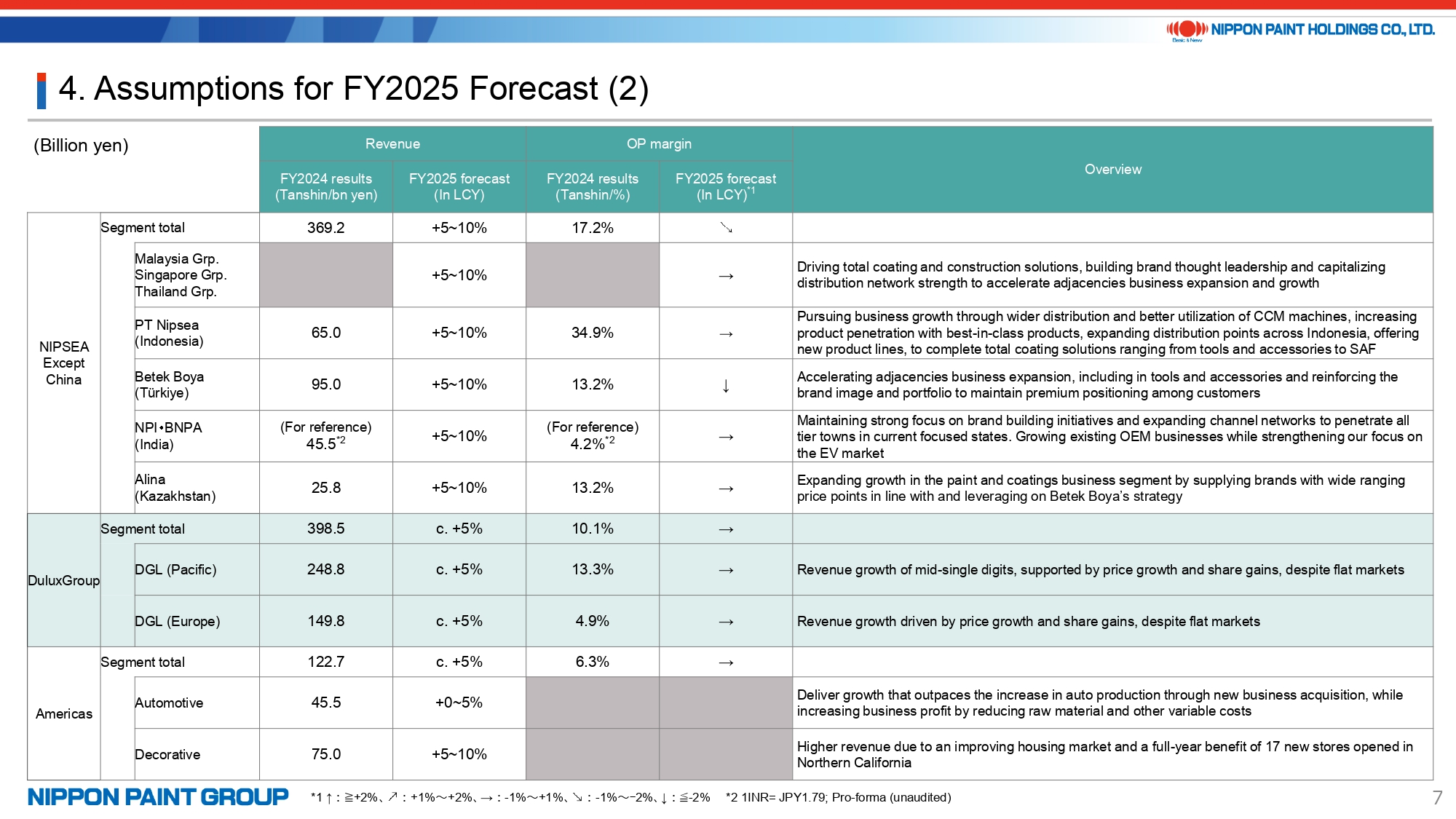

6. Assumptions for FY2025 Forecast

Pages 6 and 7 provide an overview of the key assumptions underlying our FY2025 guidance for major segments. While we will cover the details during the Q&A session, I’d like to briefly highlight each segment.

- Japan Segment: We remain focused on improving margins. However, in FY2025, we expect margins to remain flat due to expenses related to the renewal of our ERP system and costs associated with the completion of the new Research Institute at our Shinagawa Office. That said, our medium- to long-term margin target of 15% remains unchanged.

- NIPSEA China: Given the expectation that the challenging macroeconomic environment will continue, we will maintain our growth strategies with a strong focus on the TUC segment. For the TUB segment, which faced headwinds in FY2024, we will prioritize diversifying revenue streams by expanding our presence in infrastructure, public housing, and government-related projects, aiming for both growth and profitability improvements.

To reiterate, we are forecasting overall NIPSEA China revenue growth of 5–10% on a like-for-like (Apple-to-Apple) basis. - NIPSEA Except China – India Update: In FY2024, our India businesses contributed two months of earnings—November and December. For FY2025, we expect a full-year earnings contribution. Since the buyback announcement in 2022, the decorative paints market has seen more new entrants than we initially anticipated, putting pressure on our market share in the two key states where we operate. However, we have made significant progress in strengthening our position in the industrial and automotive segments. For the overall India business, we are forecasting full-year revenue growth of 5–10%, with margins expected to remain flat compared to the previous fiscal year.

- DuluxGroup: We are forecasting approximately 5% revenue growth in both the Pacific and Europe segments, driven by price increases and market share expansion amid largely flat market growth. In France, a key market for Cromology, market conditions have remained stagnant for two consecutive years. However, we remain optimistic about a potential market recovery in the near term.

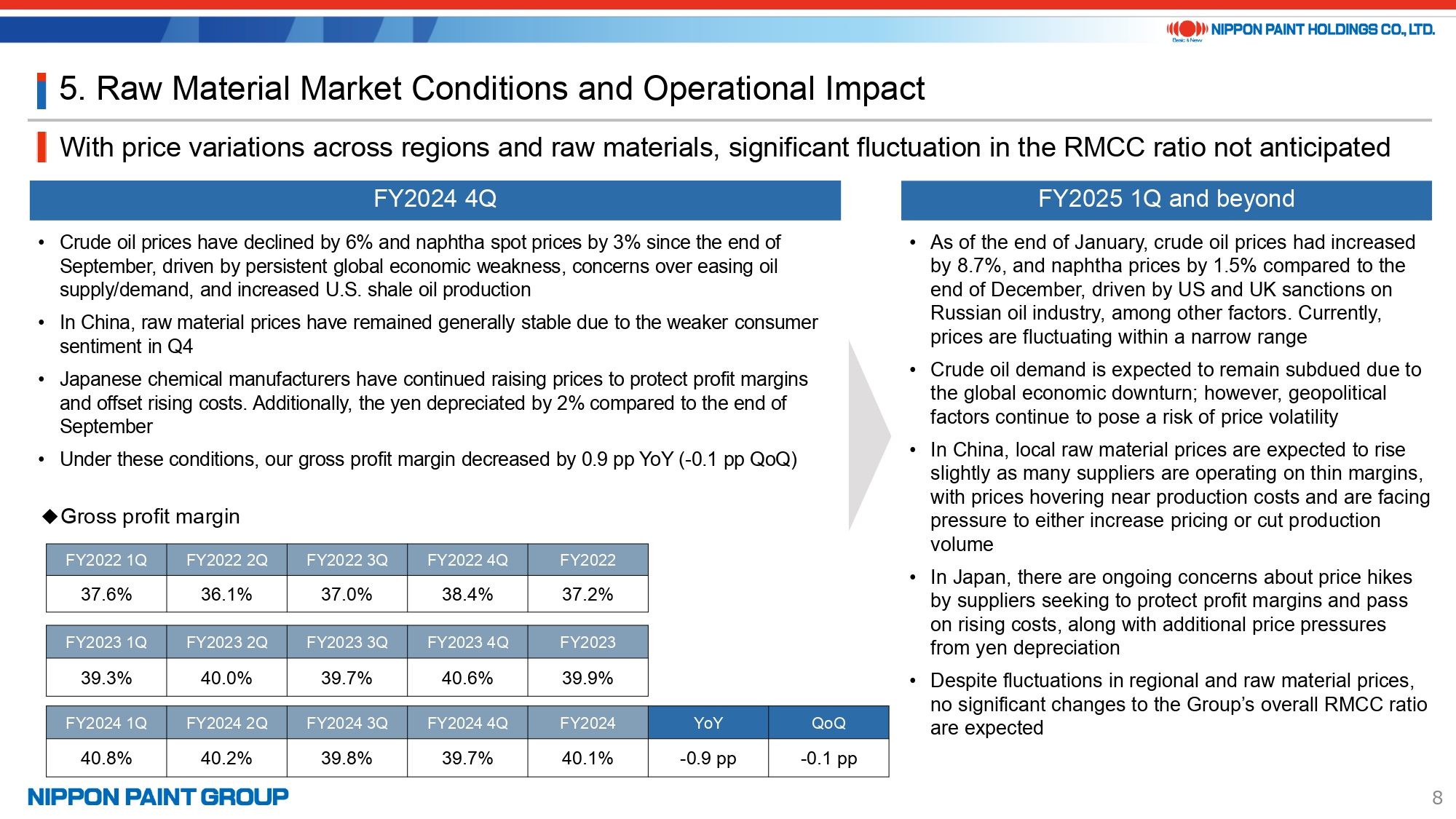

7. Raw Material Market Conditions and Operational Impact

The overall raw material market remains relatively stable; however, as anticipated, several factors could lead to fluctuations. Our base scenario assumes that market conditions will remain flat or see a slight decline.

8. Major Topics (1)

I will skip pages 9 and 10 of the presentation and proceed directly to the topics covered on pages 11 and 12.

As mentioned earlier, the closing conditions for AOC’s acquisition are progressing smoothly and could be met as early as the end of February. We continue to engage with AOC’s management on various matters, including monthly performance updates and the FY2025 budget. At this stage, there is no change to our previously announced expectation of an “EPS contribution of 15–17 yen on an annualized basis,” as stated during the acquisition announcement in October 2024. However, a detailed review will be required post-closing, particularly to account for seasonal performance fluctuations and the impact of purchase price allocation (PPA). Once these pre-acquisition assumptions are refined with post-closing adjustments, we aim to revise our earnings forecast at the earliest possible opportunity.

On December 2, 2024, we hosted our inaugural “IR DAY.” As part of our ongoing efforts to bridge the perception gap in the capital markets, DuluxGroup’s CEO and NIPSEA Group’s Brand Director provided fresh insights into our strategies and approach to the brand business in decorative paints, building on our previously outlined vision. The event was very well received by investors. For those who have not yet had the opportunity to review the materials, I encourage you to visit our IR website, where the scripts and presentations are available.

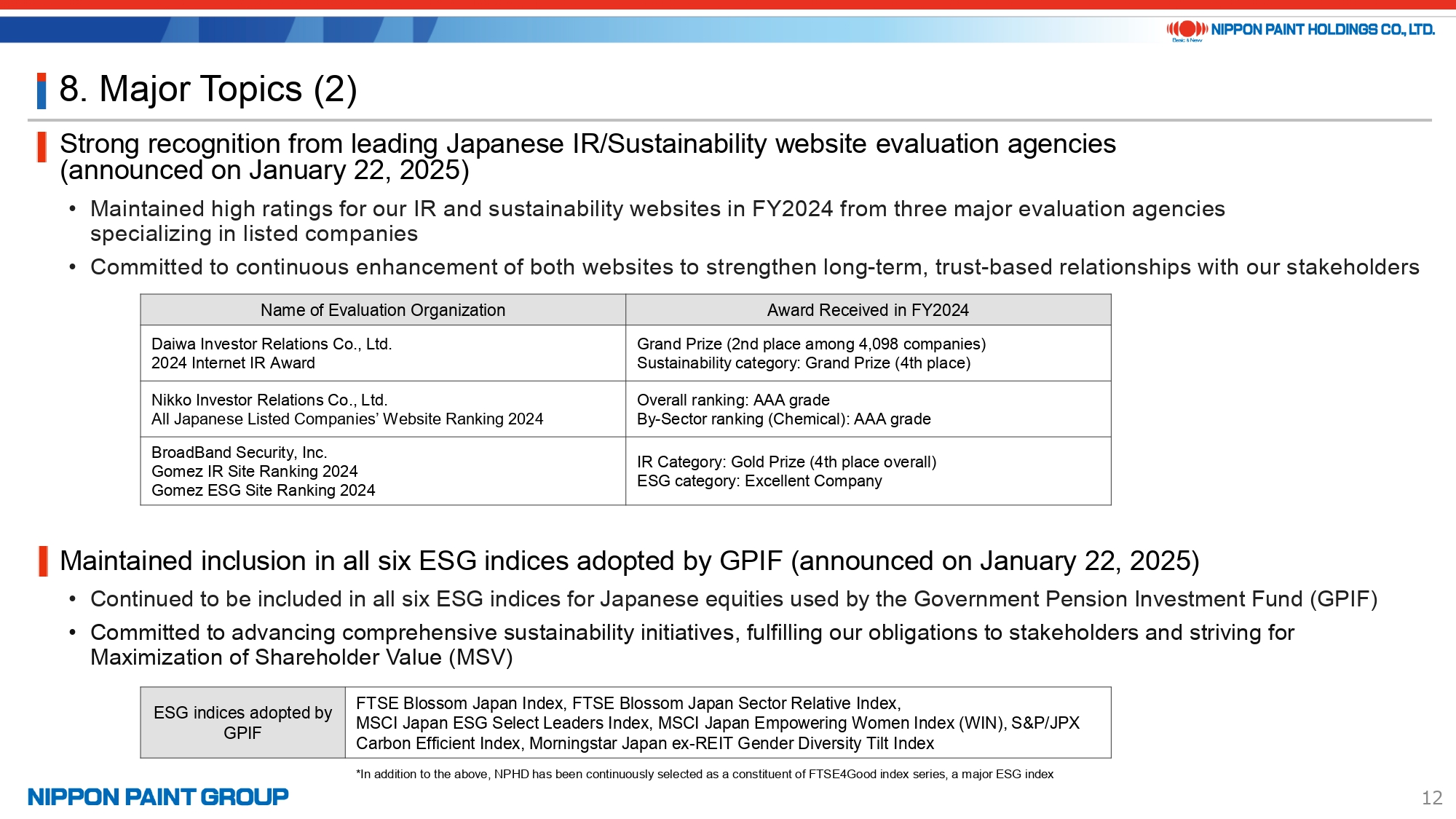

9. Major Topics (2)

Now, let me move on to the key topics announced in January 2025.

First, we received high recognition from three leading IR and sustainability website evaluation agencies. Second, following our inclusion in 2024, we have once again been selected as a constituent of all six ESG indices adopted by GPIF.

To reiterate, Maximization of Shareholder Value (MSV)—our sole mission—is the pursuit of maximizing shareholder value after fulfilling our obligations to stakeholders, including legal, social, and ethical responsibilities. We consider ESG and sustainability to be integral to these stakeholder commitments, and we are honored that our efforts in these areas have been highly recognized by external evaluation agencies.

Reflecting on 2024, we delivered strong financial results despite a highly challenging environment, reaffirming the strength of Nippon Paint Group as an assembly of exceptional partner companies. While it is unfortunate that we were unable to provide FY2025 guidance inclusive of AOC, we view 2025 as a pivotal year—the starting point where we can fully demonstrate the power of our Asset Assembler model. This approach harnesses both the sustainable growth of our existing businesses and M&A activities that drive EPS accretion from the first year. We appreciate your continued support and look forward to advancing even further together.

Lastly, I am pleased to announce that we will be hosting an update briefing on the Medium-Term Strategy announced in April 2024. The briefing is scheduled for Thursday, April 3, from 16:00 to 17:30 JST, and we warmly invite everyone to participate.

Thank you for your time and attention.