Font Size

1. Front Cover

Hello everyone. I’m Yuichiro Wakatsuki, Co-President of NPHD. Thank you very much for taking time to join us today while you are busy, despite the sudden notice.

I would like to take a moment to explain about the acquisition of US-based AOC, which was announced today.

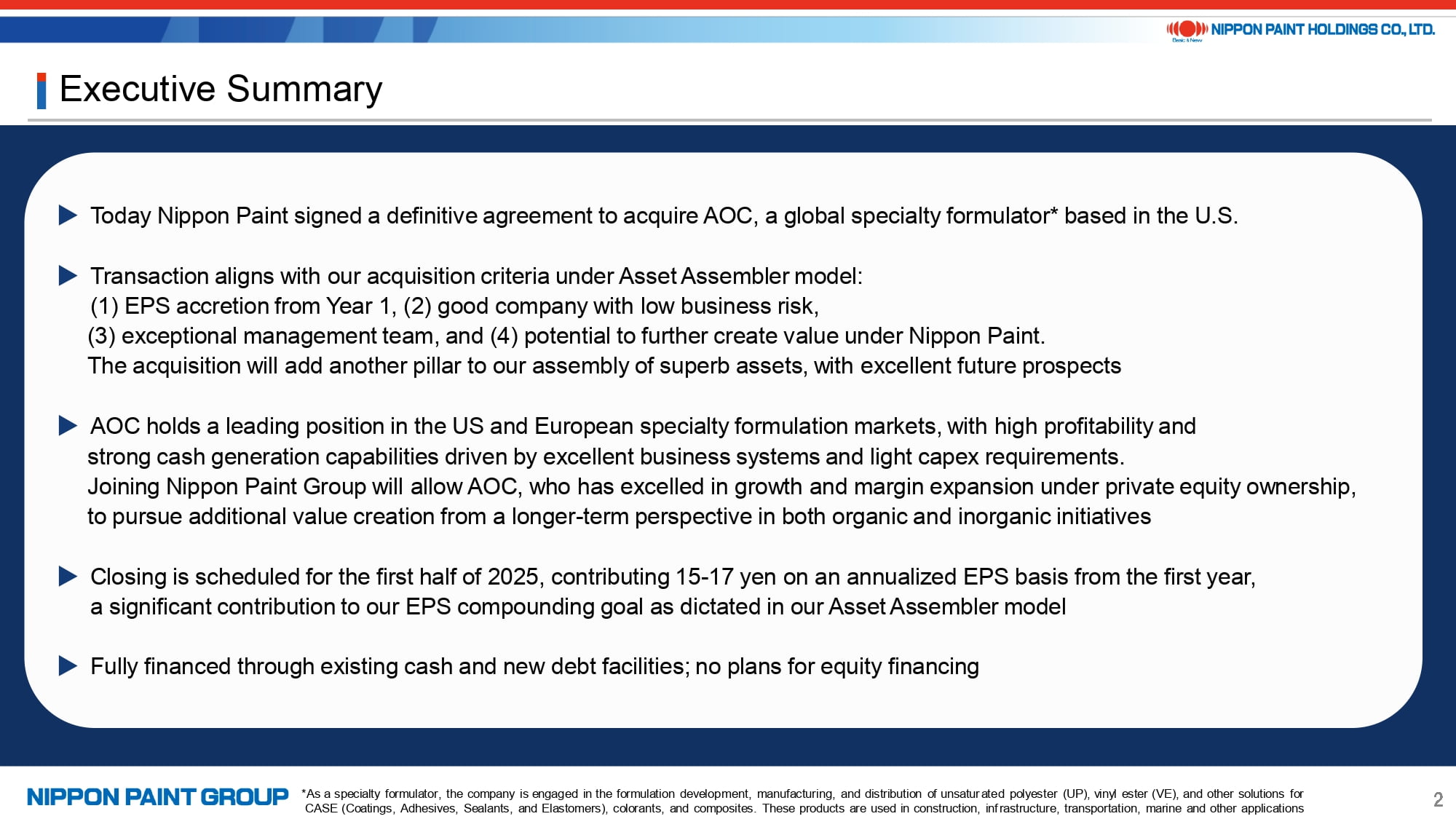

2. Executive Summary

Let’s start with today’s summary.

The acquisition target is a U.S. based global specialty formulator. Specialty formulator means the company is engaged in the formulation development, manufacturing, and distribution of unsaturated polyester (UP), vinyl ester (VE), and other solutions for CASE (Coatings, Adhesives, Sealants, and Elastomers), colorants, and composites. These products are used in construction, infrastructure, transportation, marine and other applications.

This acquisition is aligned with the asset assembler model that we have been talking about as part of our growth strategy, and in a sense, we believe that this embodies our future vision. As a leading company with a strong and resilient business model, AOC will be added as a new pillar to NPHD Group, contributing to EPS from year one post-acquisition without relying on any synergies. AOC is led by an excellent management team with a track record of significant value creation which we expect to accelerate under NPHD Group. This transaction is a significant milestone which establishes a major pillar for NPHD since the acquisition of DuluxGroup in 2019.

AOC has a leading position in the U.S. and European markets and has developed business systems that help generate a highly profitable business with strong cash generation capabilities, backed by low capital expenditure requirements as we will explain later. AOC has achieved substantial profit growth in a disciplined manner under the ownership of multiple private equity firms. We are confident that we will be able to pursue further value creation from a longer term perspective without being constrained by short term exit strategy. We have been in close communication with AOC management, and we are all very excited about future growth opportunities.

The closing is scheduled for the first half of FY25 after the achievement of certain regulatory approvals customary to a deal of this nature. EPS is expected to increase by approximately 30%, which is 15 to 17 yen, compared to the pre-acquisition level on an annualized basis, based on various assumptions at this point of time.

The acquisition cost is funded through cash on hand and debt. There is sufficient leverage capacity, and we do not have any plans for equity financing in connections with this transaction.

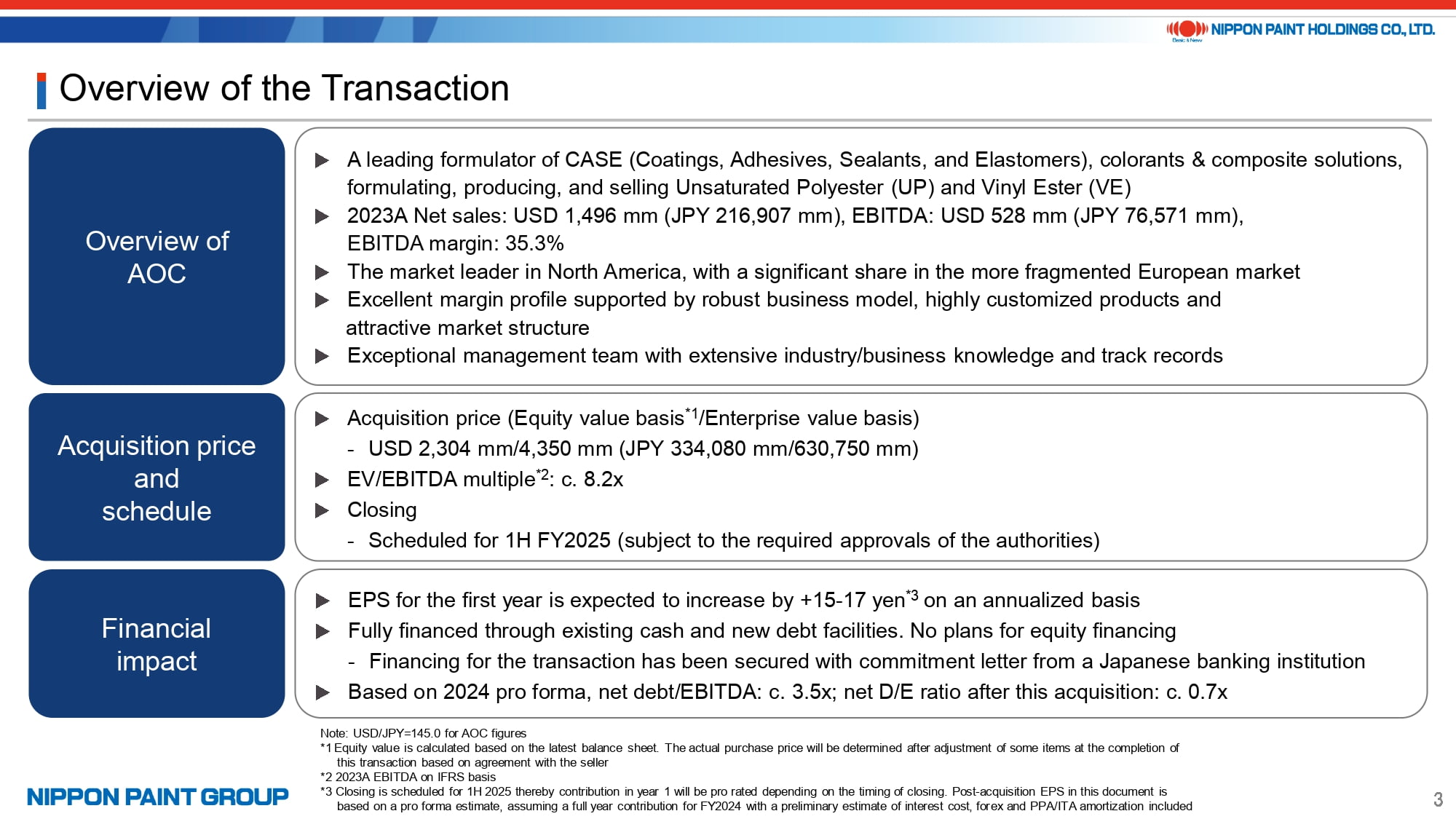

3. Overview of the Transaction

P3 provides an overview of the transaction.

In 2023, AOC’s net sales were approximately $1.5 billion, EBITDA was approximately $530 million, with an EBITDA margin of approximately 35%. In both North America and Europe, AOC has built a strong market position, and the key point is that, like the paint and coatings industry, AOC boasts strong local presence that allows for superior local customer service, which is further bolstered by its robust technical service capabilities and deep understanding of its customers’ businesses. We believe these capabilities establish a strong competitive advantage that helps drive AOC’s excellent performance by focusing on customized, high-value-added products. In particular, a very good management team led by CEO Joe Salley, who joined the company in 2018, has achieved this performance, and we have confirmed that they will continue to manage the company after the completion of this transaction.

The purchase price is approximately $4.35 billion, including debt and EV/EBITDA multiple is approximately 8.2 times against 2023 EBITDA.

We already touched upon the financial impacts, but in terms of leverage capacity, Net Debt/EBITDA would be about 3.5x and the Net DE ratio would be 0.7x in 2024 on a pro forma basis, which are in the safe zone that we have been talking about before. In fact, AOC’s capital expenditure requirements are 2-3% of sales, which is the same level as in the paint and coatings industry, with more attractive margins than in the paint and coatings industry. We therefore believe that leverage would not be a problem at all.

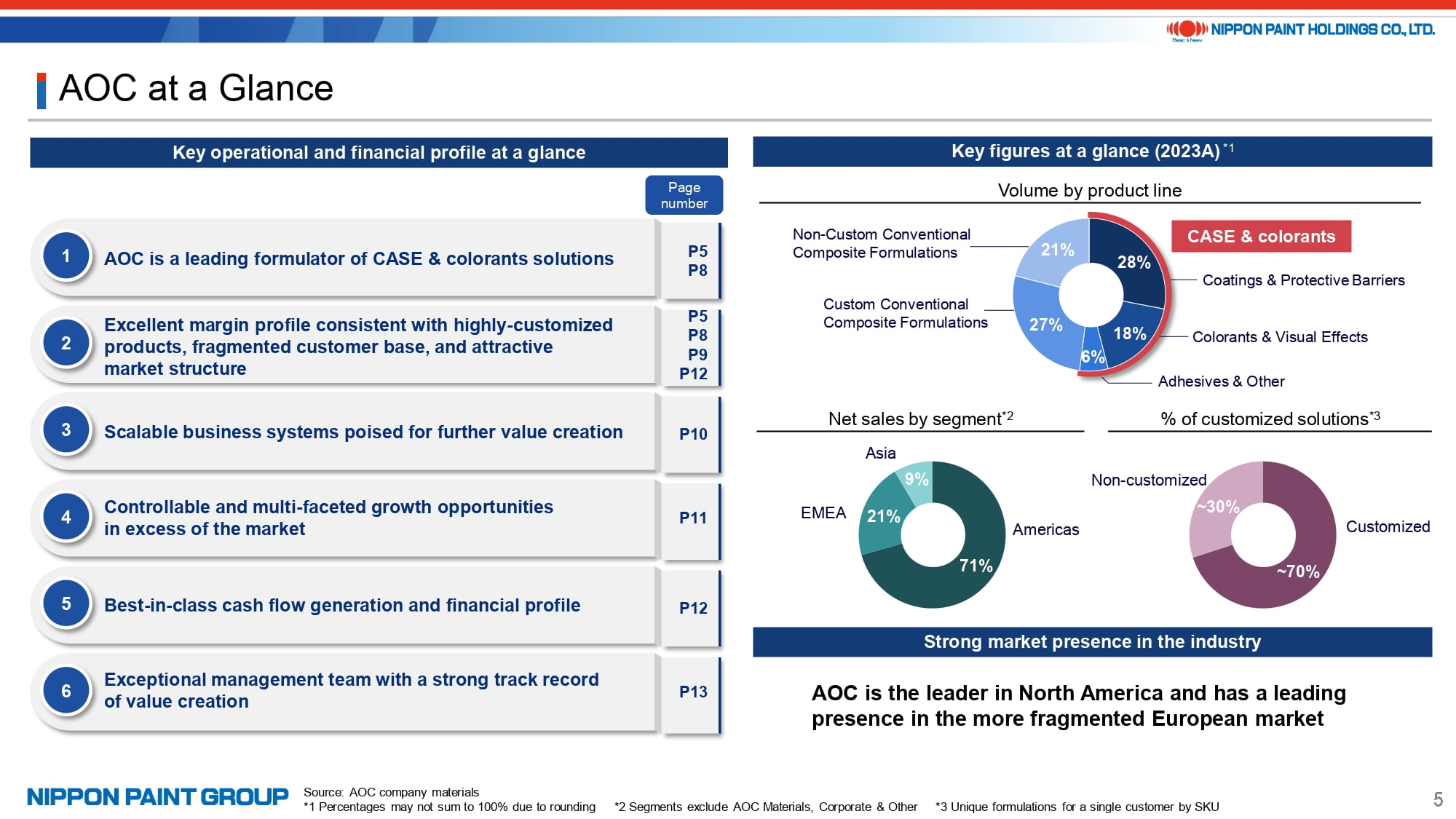

4. AOC at a Glance

Next, we would like to explain a little bit more about AOC.

We have already mentioned key operational and financial profile of AOC, and we would like you to highlight on the right side is that about 70% of AOC’s products are custom formulations. AOC’s formulations are proprietary and confidential, and its capabilities allow it to meet customer needs and differentiate itself from competitors by providing higher performance solutions. In addition, the Americas account for 70% of the total sales, and Europe is still modest, but we believe has substantial room for further growth.

The customer base is also diversified, with about one-third of sales relying on the top 10 customers.

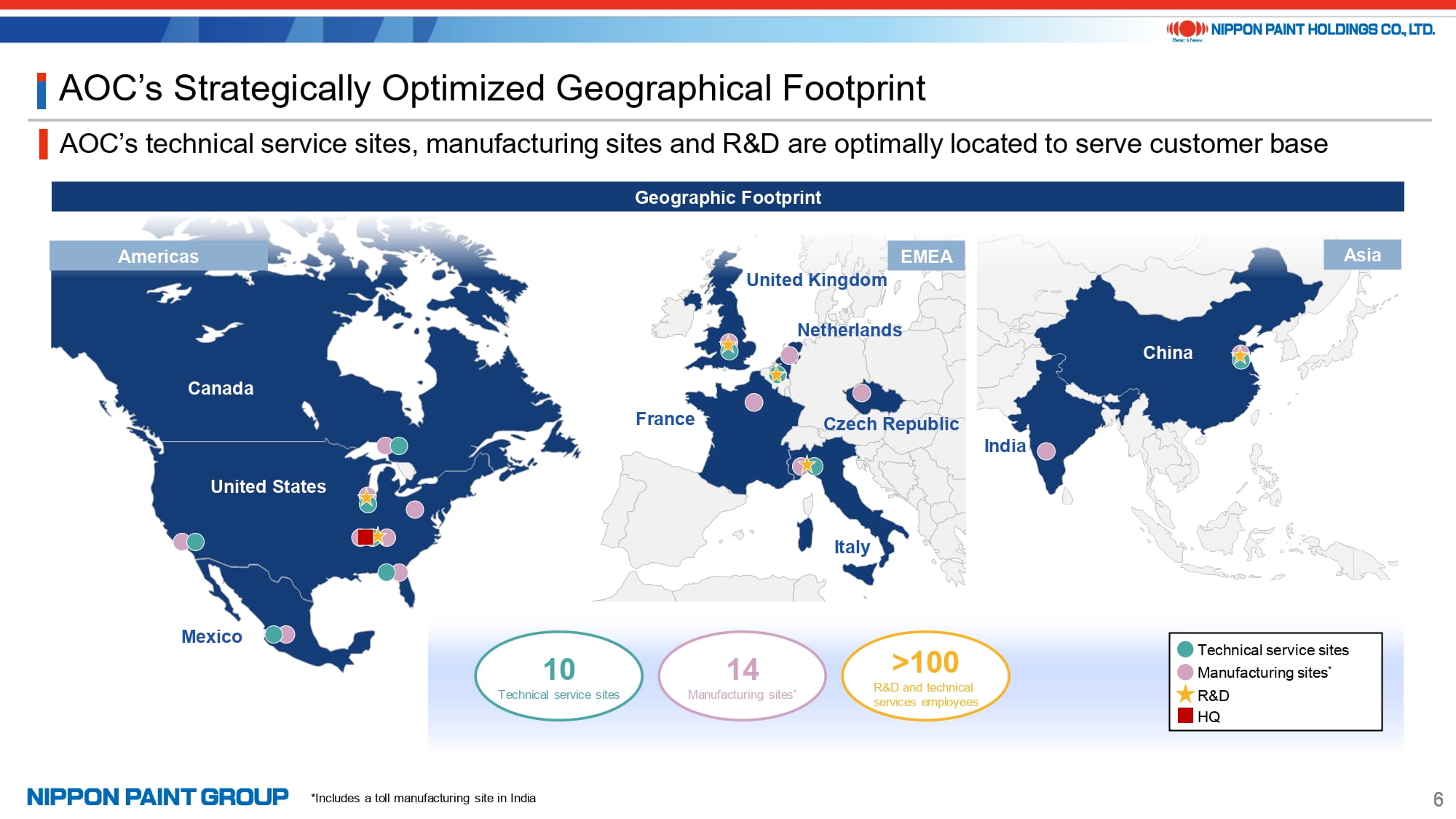

5. AOC’s Strategically Optimized Geographical Footprint

In terms of AOC’s global footprint, AOC has 14 manufacturing sites and 10 technical service sites around the world, and these are close to its customer locations. AOC focuses on providing added value through products tailored for local needs, strong product delivery capabilities that meet challenging customer requirements, and local technical service.

6. Solutions Used in Everyday Products Critical to Daily Living

As you can see here, AOC serves a fairly wide range of applications and end markets.

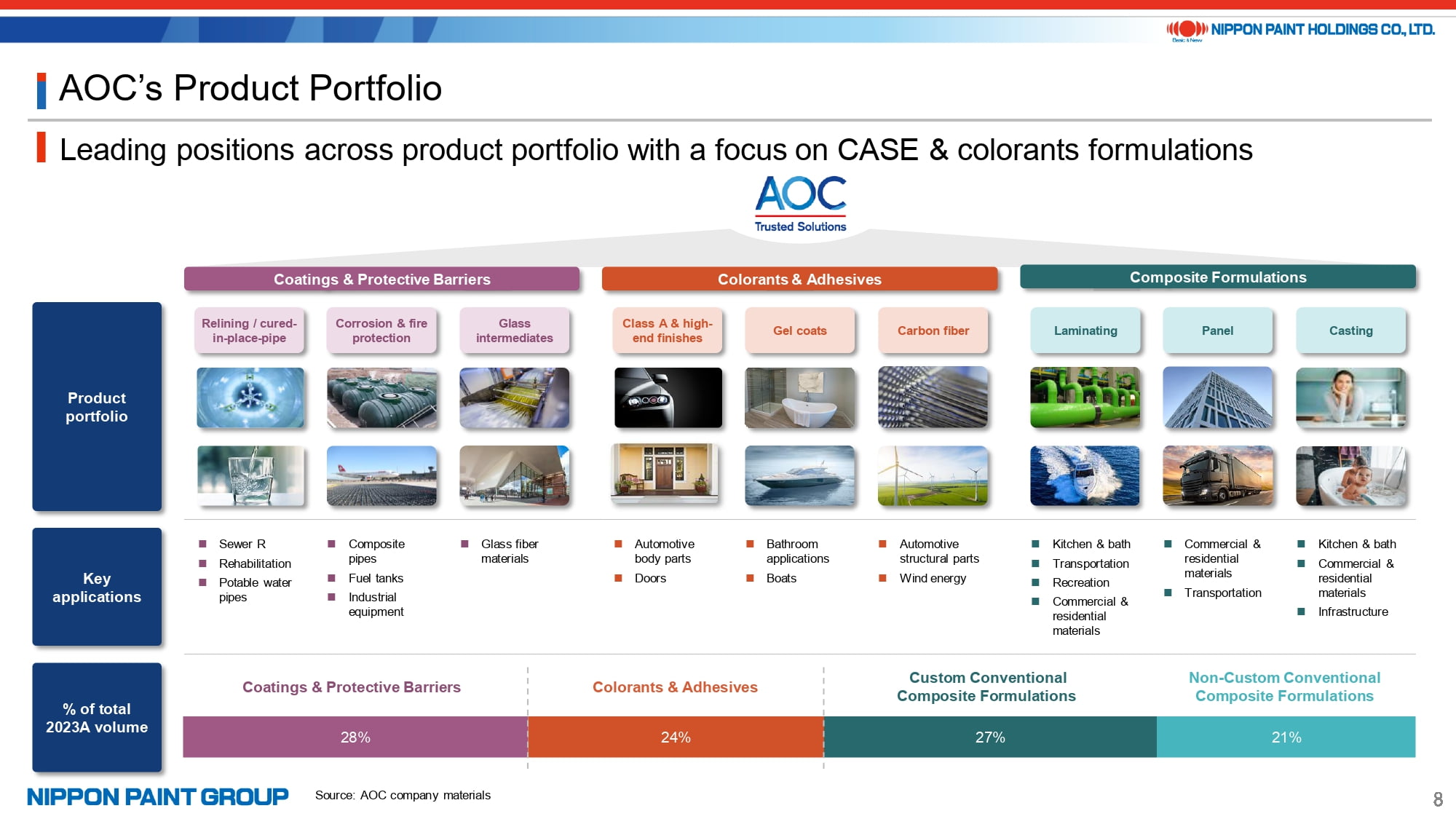

7. AOC’s Product Portfolio

On this slide, we show examples of AOC’s diversified product portfolio.

As you can see, their products cover a wide range of end markets, and some of these end markets are influenced by business sentiment and interest rates. Other markets, such as infrastructure, are not dependent on the business cycle, and there is definitely a need for infrastructure investment and development in the U.S. that we believe will drive growth in the medium to long term.

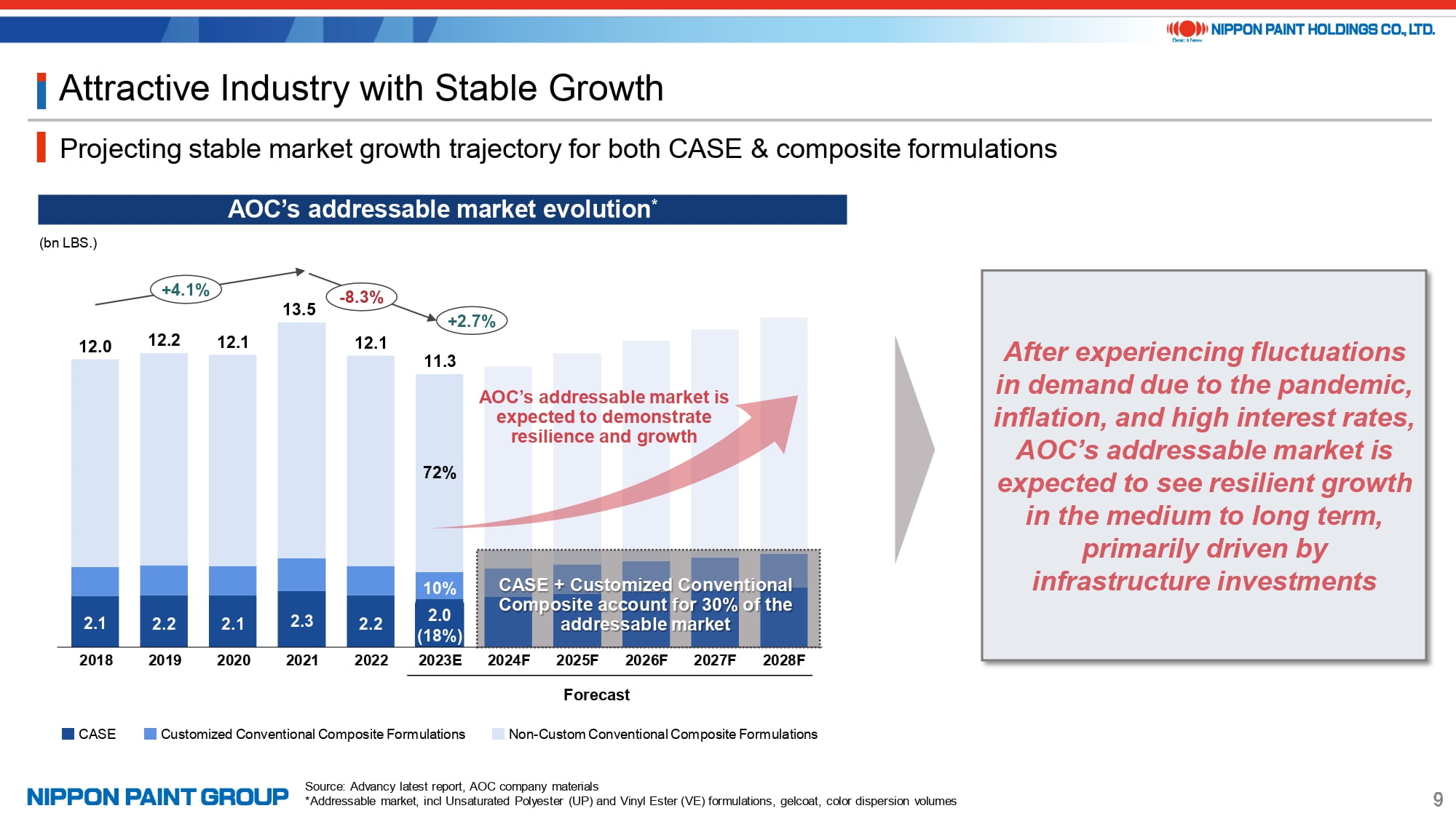

8. Attractive Industry with Stable Growth

In terms of market size, so-called non-customized composite formulations market is larger, but AOC focuses on the CASE & Customized Conventional Composite market, which accounts for about 30%. The market has been volatile in the past few years due to COVID, supply chain disruption, inflation, and high interest rates, but that the market is expected to grow resiliently in the medium to long term.

In addition, AOC has an excellent track record of generating solid profits in fluctuating economic environments.

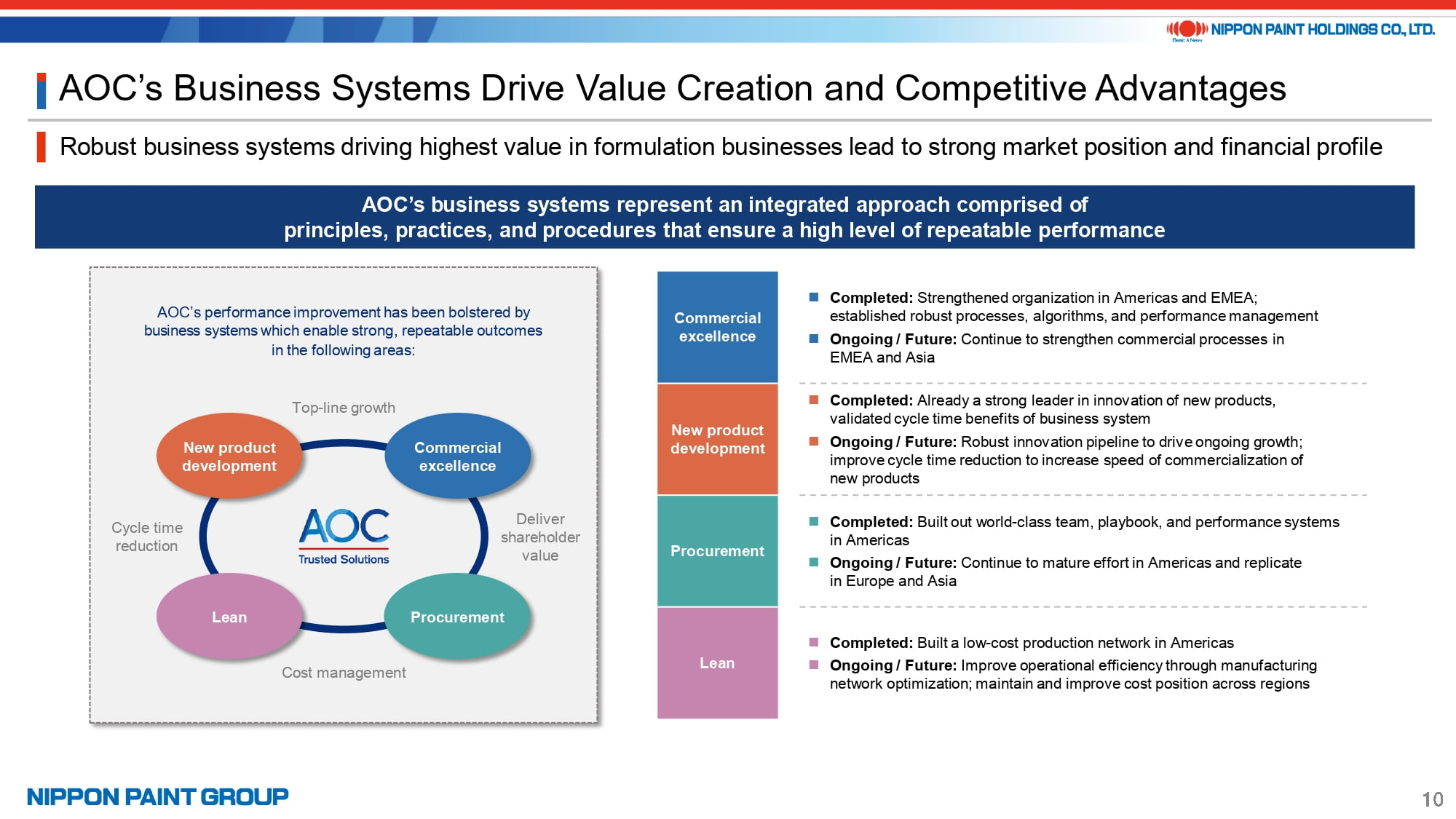

9. AOC’s Business Systems Drive Value Creation and Competitive Advantages

Here, we would like to briefly explain about AOC’s business systems, which is one of the major drivers of their added value.

It is basically a holistic approach that traces its origin back to the Toyota Production System and is comprised of principles, practices and procedures that ensure a high level of repeatable performance. While it is used by many companies, AOC applies it systematically to improve business in a determined manner. AOC teams work together to continuously improve value by looking at important areas, such as new product development, lean manufacturing, procurement, and commercial excellence, from multi-faceted perspectives.

I think that NPHD, which is already operating with a high level of cost awareness, can learn a lot from this approach.

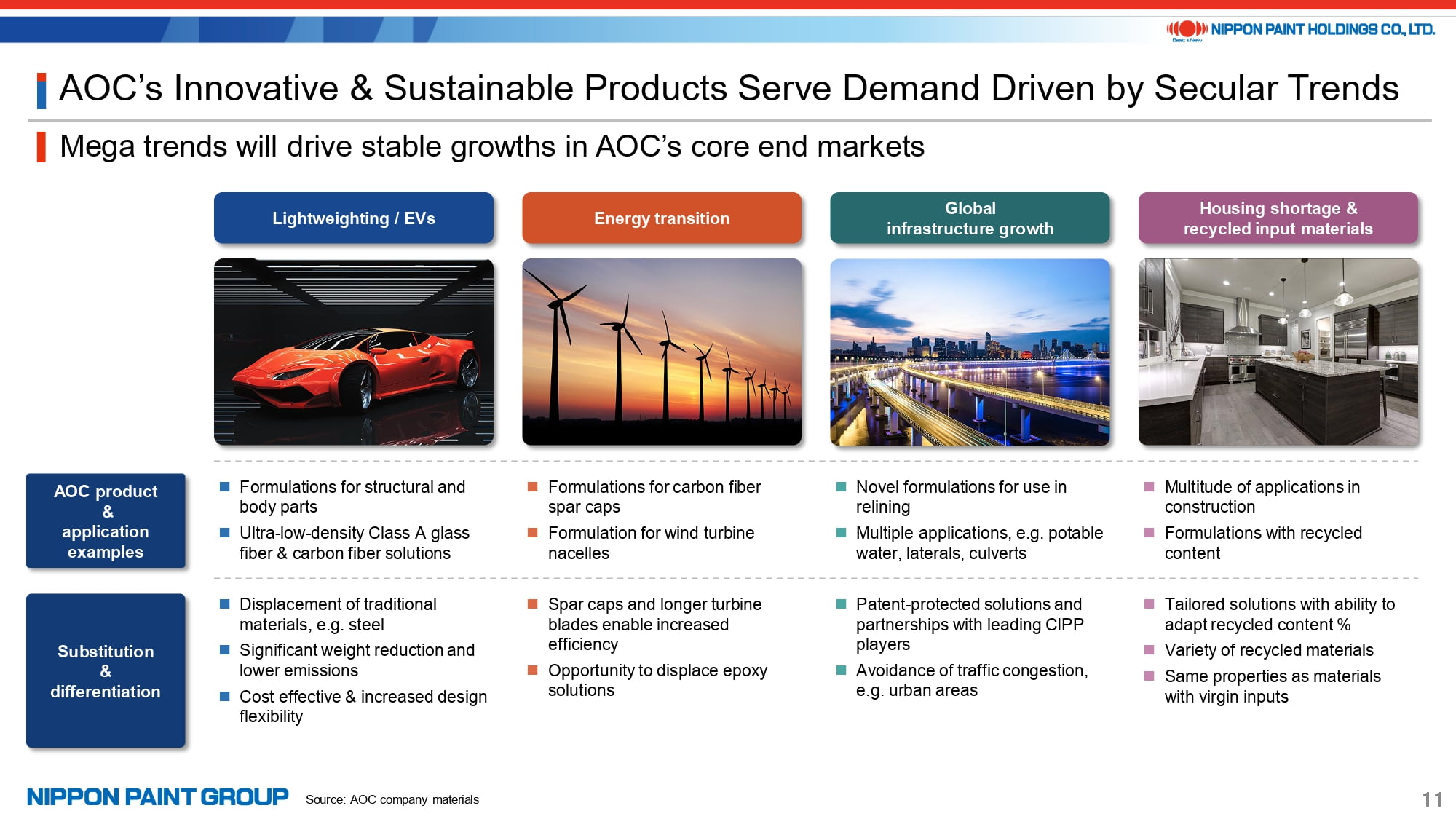

10. AOC’s Innovative & Sustainable Products Serve Demand Driven by Secular Trends

In the medium to long term, we expect not only a recovery in business sentiment but also various trends to support market growth. Lightweighting, Energy Transition, Infrastructure Growth, and Housing Shortages will drive demand, albeit depending on the timing of certain market events We believe that AOC’s innovative products will continue to provide a variety of added value and bring about growth, including the ability to open new markets for its products via the replacement of traditional materials.

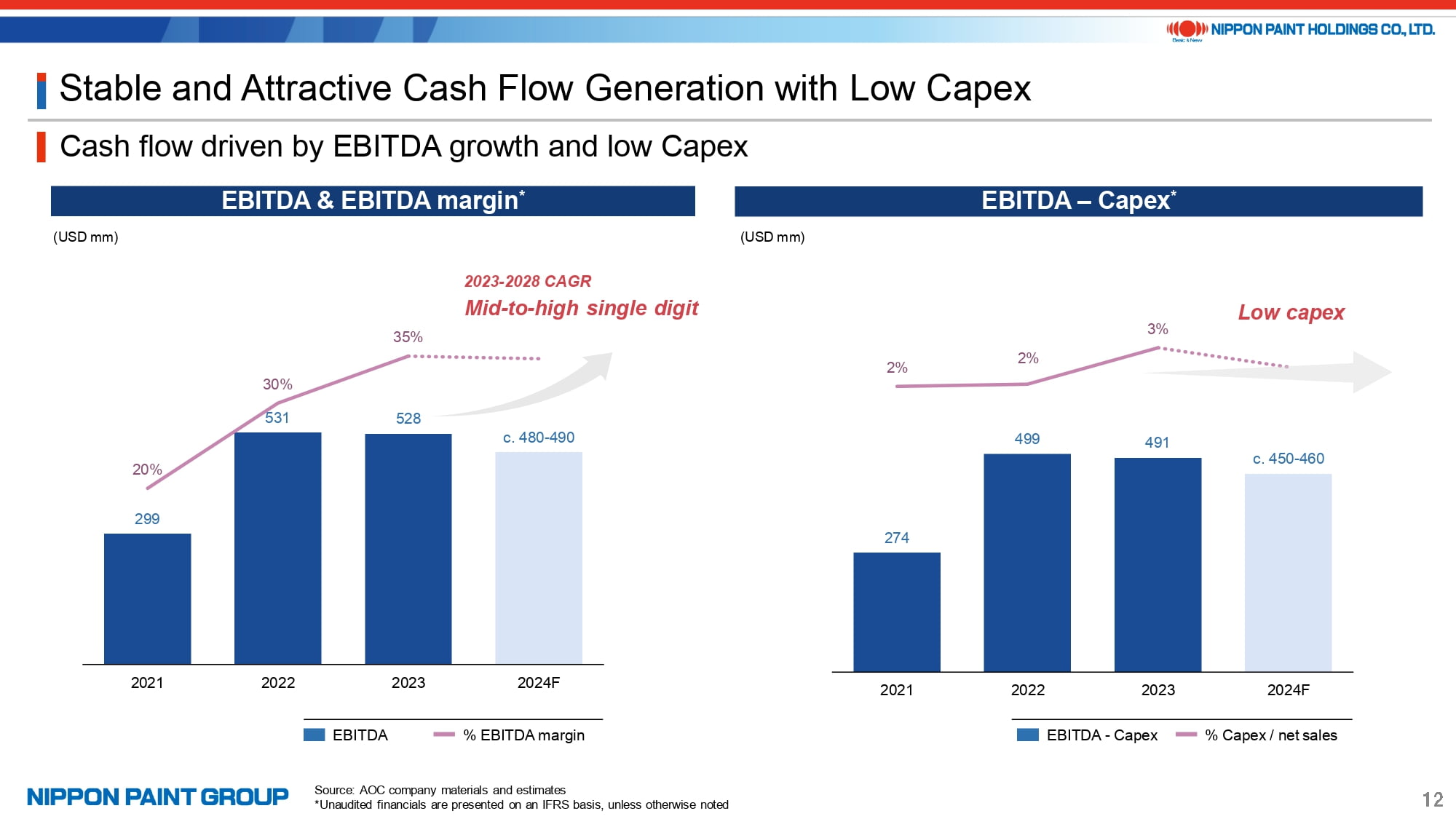

11. Stable and Attractive Cash Flow Generation with Low Capex

As we have mentioned so far, AOC demonstrates robust profitability. After the increase in demand after COVID, market demand decreased sharply in 2022 and 2023 due to destocking and the general economic environment. AOC did an excellent job in improving and maintaining its profitability. Over the medium term, we expect mid-to-high single digit volume growth.

12. Exceptional Management Team with a Track Record in Driving Value Creation

Wee Siew Kim and I had meetings with several other members of the management team in addition to those listed here, and we both confirmed that they are all highly motivated and aim to create value as a team.

We look forward to working with AOC’s CEO, Joe Salley, who has shown the strong ability to lead such an excellent team.

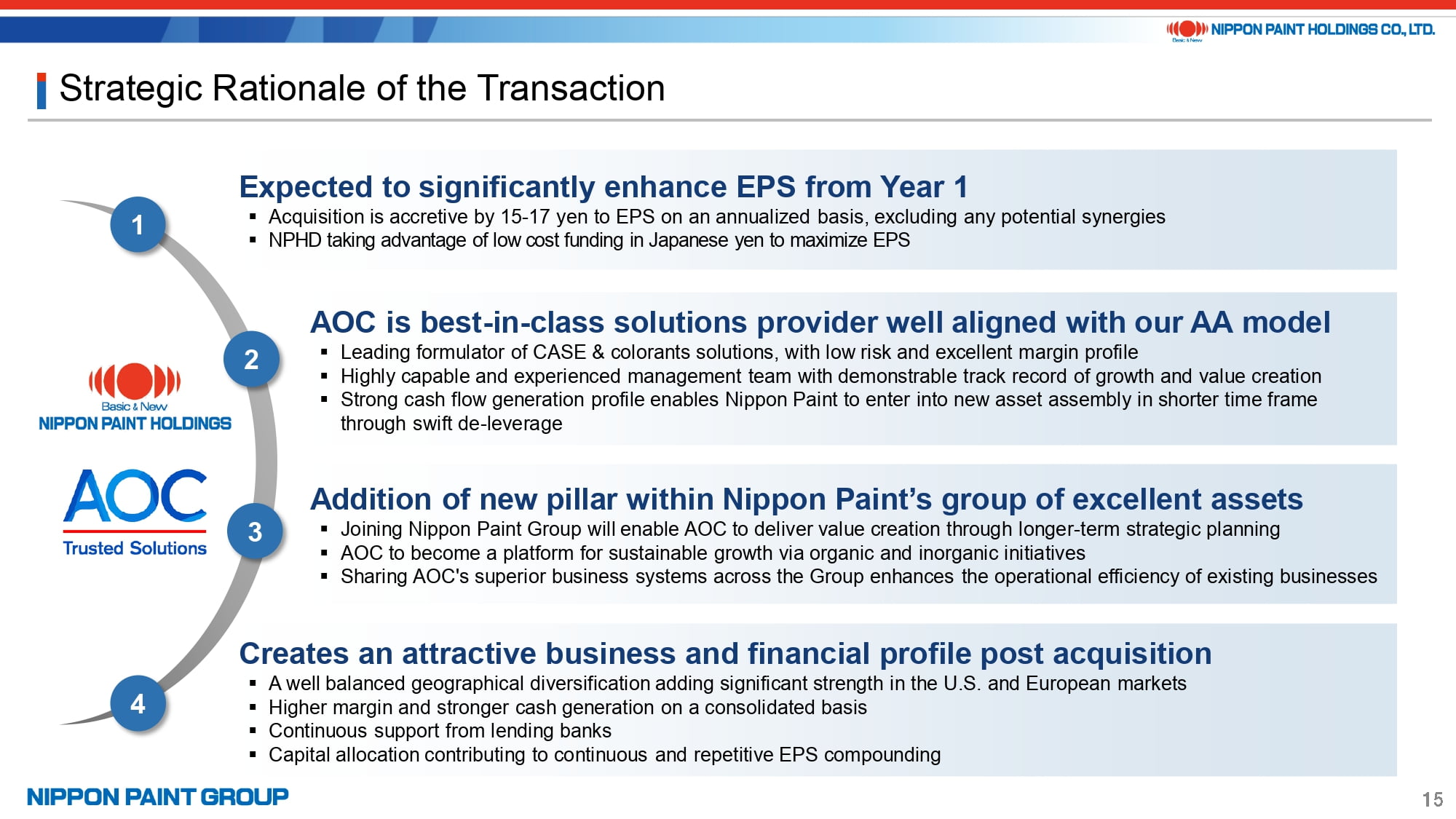

13. Strategic Rationale of the Transaction

This is where we will explain more about the strategic rationale of this transaction, but we have already outlined it so far, so we will not repeat it too much.

- Essentially, we will pursue various synergies, but the point is that even without synergies, we will be able to increase EPS safely and significantly.

- Thanks to the high cash generation capabilities, deleveraging is expected to proceed quickly, and although we may not immediately carry out large-scale M&A which will bring about the next pillar, we always seek an opportunity for the next target. We will seek opportunities for bolt-on M&A every year.

- Just like DuluxGroup, great companies will take advantage of our platform and seek additional opportunities for growth, and NPHD encourages that. In that sense, we will pursue additional M&A at the holding company level as well as additional M&A at the AOC level, provided that the risk and return are justifiable.

- As we have stated before, we will prioritize growth investments over short-term returns, and we will continue to make capital allocations that contribute to EPS compounding. However, it is important to note that M&A itself is not the goal, but the safe EPS compounding and the maximization of EPS are key.

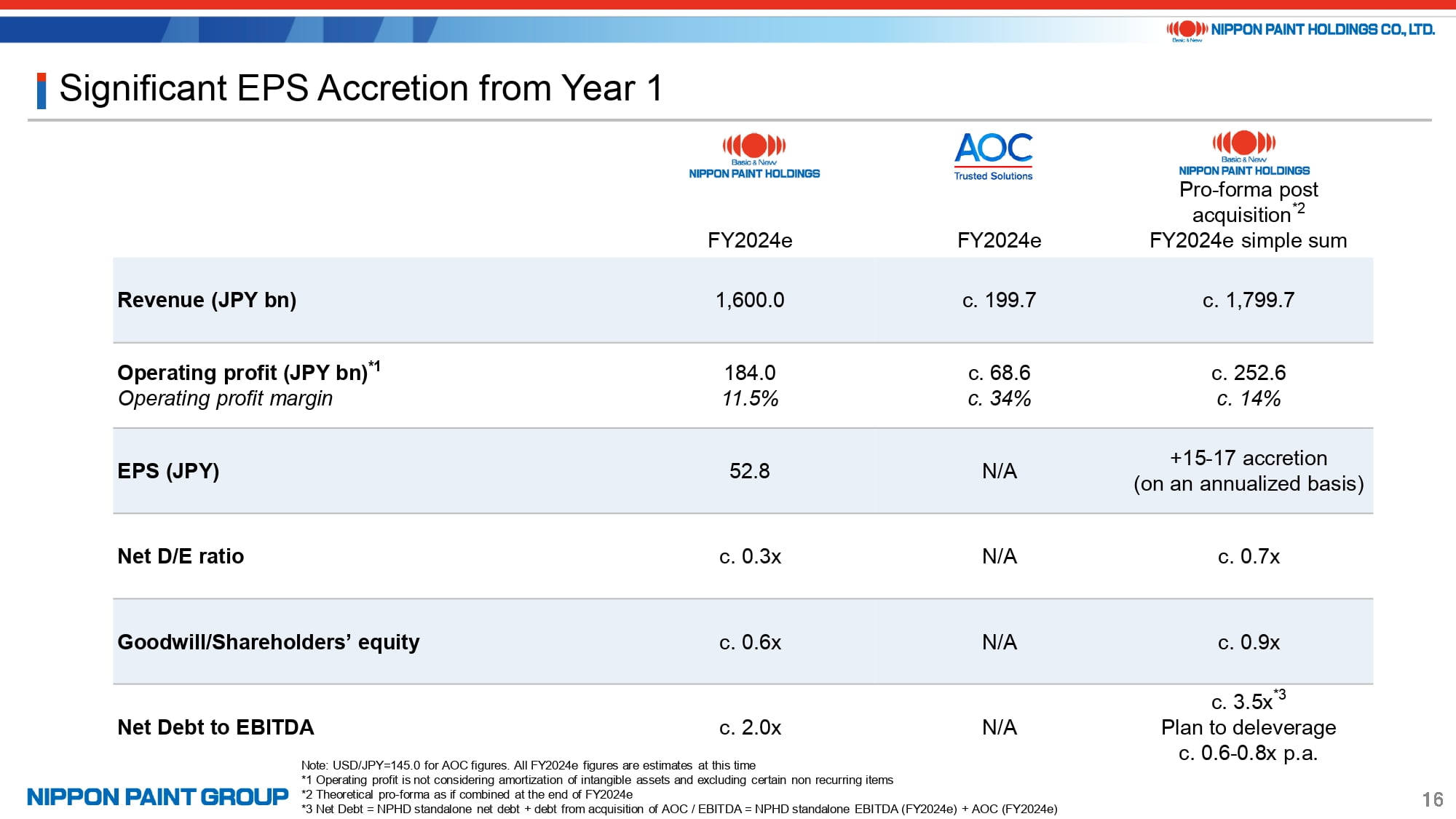

14. Significant EPS Accretion from Year 1

This is an overview of the pro forma calculation. The figures for 2024 are only rough estimates and forecasts at this point of time, so please be mindful that these figures are based on various assumptions.

15. Asset Portfolio

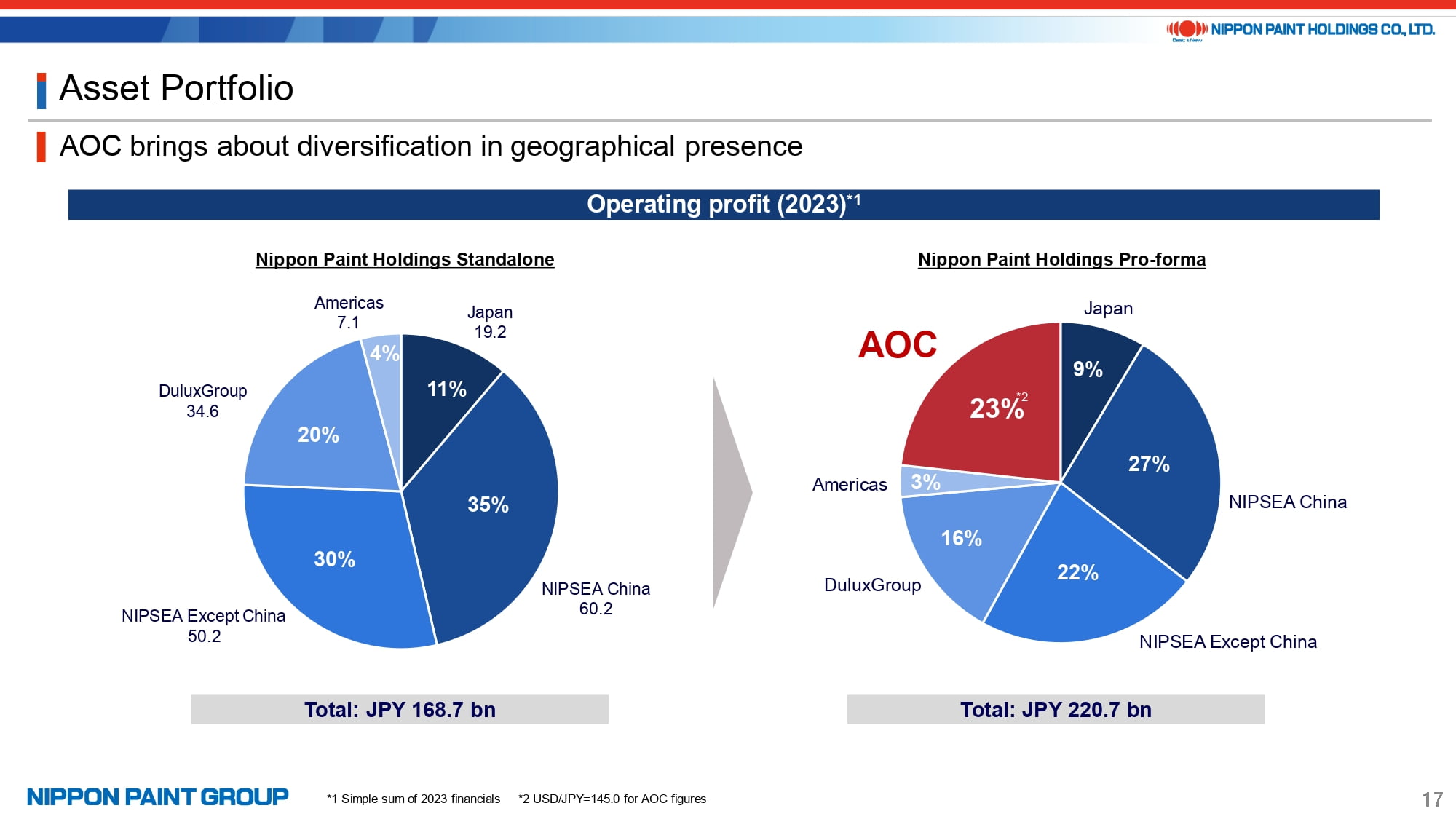

This is an illustrative overview of operating income breakdown by region before and after this acquisition based on 2023 figures.

As you can see, AOC is one of the major pillars along with NIPSEA China, NIPSEA except China and DuluxGroup.

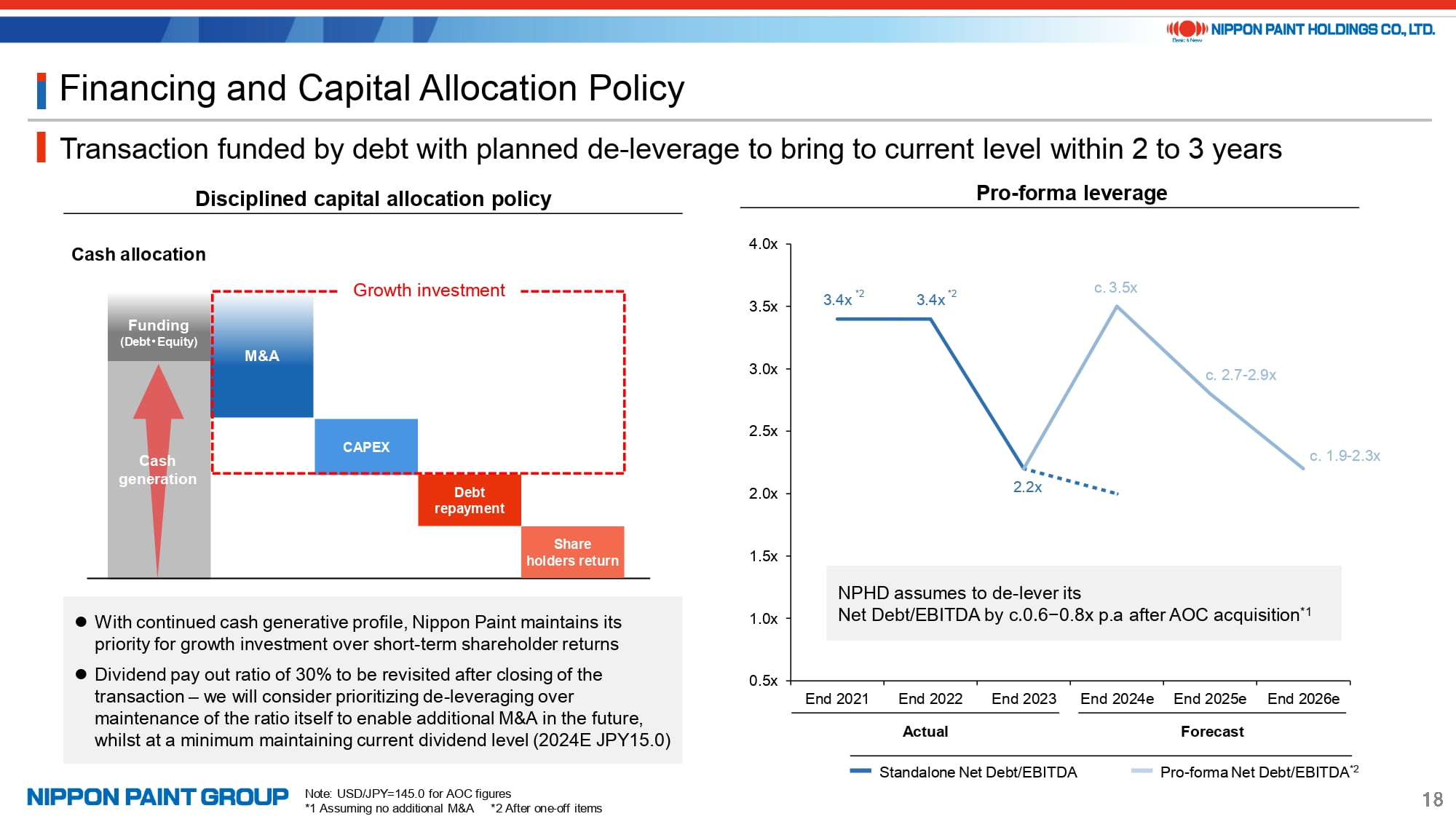

16. Financing and Capital Allocation Policy

This is an explanation of the state of capital. On the right-hand side, this is a simulation without new bolt-on M&A etc., but it is assumed that deleveraging equivalent to 0.6 ~ 0.8x Debt/EBITDA per year can be achieved. That is why we expect that we will be able to return to the current leverage level in about two years.

In terms of capital allocation, in view of the fact that EPS can increase to such an extent through asset assembly, we believe that the dividend payout ratio of 30% should be revisited after closing. At the very least, we will maintain the current level of the dividend payout ratio, but we believe that reducing outflows of cash and preparing for the next acquisition will help MSV in the medium term.

17. Summary

In summary, this acquisition is a true embodiment of the asset assembler strategy that we have been pursuing since 2022. By utilizing low funding costs in Japanese yen, we can significantly increase EPS from the first year, and the asset can grow autonomously.

As we have stated before, there is nothing to impede the issuance of shares and it is an option for fundraising, but we believe that we should first aim for the next acquisition, focusing on lower debt costs, by reducing leverage at an early stage, and we believe that it is quite possible to continue such acquisitions after deleveraging.

In addition, through our interactions with the seller and the management of AOC, we were able to gain alignment with the simple but powerful mission of MSV, including the path to future value creation. By becoming a long-term shareholder of a good company, we would like to further realize MSV.

In that sense, although this is a very large acquisition, our stance of pursuing both organic and inorganic growth has not changed at all, and we will do our best to meet your expectations for future deliveries of values.

This concludes my presentation, and I would like to take questions from all of you. Thank you for your attention.